Project Management: Cost Management

Project Cost Management

- Resource Planning – Determining what resources (people, equipment, materials) and what quantities of each should be used to perform project activities.

- Cost Estimating – Developing an approximation (estimate) of the costs of the resources needed to complete project activities.

- Cost Budgeting – Allocating the overall cost estimates to individual work activities.

- Cost Control – Controlling changes to the project budget.

- The four processes within cost management are:

- Plan cost management

- Estimate costs

- Determine budget

- Control costs

Here we make sure the project is completed within the approved budget. It incorporates four areas:

-

Resource planning - as noted above but with an emphasis on what is the most cost effective (within your risk tolerance level) method of obtaining the needed resources

-

Cost estimating - coming up with an approximate estimate of overall costs (coined life-cycle costing)

-

Cost budgeting - allocating the overall cost estimate to individual work activities

-

Cost control - making sure the project stays on budget

Resource Planning

Why is this an important part of cost management? Well, because the resources you choose will likely vary quite a bit in their cost. If you went with external professionals for every task you will likely have a very high cost project. However, if you go with some lower cost alternatives you may be sacrificing quality, creativity, or market expertise. Another example is if you spend less time in the beginning developing the optimal design for a project product you may end up spending more that was necessary in operating or development costs.

There are seven fundamental resources you most likely will need:

- people

- money (cash versus net value should be considered)

- equipment

- facilities

- materials and supplies

- information

- technology

Cost estimating

Here you come up with the overall expected costs for the project and start to break those costs out into what will become the project budget. Basically you need to start somewhere with a budget and then refine it. Another important factor of this step is it considers the overall costs of project from start to finish so the company and the team understand the actual costs of the project up front (to the degree possible) and can earmark areas with high potential for going over budget due to high risks, high costs, or high levels of ambiguity.

Cost estimating is actually done throughout the project and often becomes more accurate as the project proceeds.

Types of estimates:

- Top down (top level estimate)

- Bottom up (by details of project and summarizing)

- Analogous (like another project)

- Parametric (cost based on a parameter)

- Definitive (variance of the sum of the details will be less significant than the significance of the variance of the details themselves)

Cost budgeting

Your intended output from cost budgeting is developing a cost baseline. A cost baseline "is a time-phased budget that will be used to measure and monitor cost performance on the project." (PMI, 2000, p. 90). In basic terms, cost budgeting is allocating cost to individual work items in the project. As described by Newell, "the cost baseline for the project is the expected actual cost of the project. The budget for the project should contact the estimated cost of doing all of the work that is planned to be done for the project to be completed. In addition, cost must be budgeted for work that will be done to avoid, transfer, and mitigate risks. Contingency must be budgeted for risks that are identified and may or may not come to pass. A reserve must be budgeted for risks that are not identified." (Newell, 2002, p. 83)

Cost control

"Cost control is concerned with a) influencing factors that create changes to the cost baseline to ensure that changes are agreed upon, b) determining that the cost baseline has changed, and c) managing the actual changes when and as they occur. Cost control includes:

- monitoring cost performance to detect and understand variances from the plan.

- Ensuring that all appropriate changes are recorded accurately in the cost baseline.

- Preventing incorrect, inappropriate, or unauthorized changes from being included in the cost baseline

- Informing appropriate stakeholders of authorized changes.

- Acting to bring expected costs within acceptable limits.

Cost control includes searching out the 'whys' of both positive and negative variances." (Project Management Institute, 2000, p. 91)

----

Newell, M. W. (2002). Preparing for the Project Management Professional (PMP) Certification Exam. New York, NY: American Management Association.

Project Management Institute (2000). A Guide to the Project Management Body of Knowledge. Newton Square, PA: Project Management Institute, Inc.

According to the Bureau of Labor Statistics, more than half of all cost estimators work in the construction industry, and another 17 percent are employed in manufacturing industries. Overall employment of cost estimators is expected to grow faster than average for all occupations through the year 2014. In addition to openings created by growth, some job openings will arise from the need to replace workers who transfer to other occupations or leave the labor force. In construction and manufacturing—the primary employers of cost estimators—job prospects should be best for those with industry work experience and a bachelor’s degree in a related field.

Cost Estimation

Conceptual cost estimating for project work (construction, industrial maintenance, etc.) is usually derived from a mix of estimating software, industry standards (formulas in books) and personal/corporate experience. Estimating software and formulas from books may produce "black box" estimates that lack qualification of one or many issues:

- What does the estimate include (prep work, indirects, clean-up, etc.)?

- What conditions are assumed (controlled environment, outdoors, etc)?

- What methodology (tools, equipment, procedure) is assumed?

- What labor proficiency (productivity) is assumed?

In these cases, estimating becomes more of an art than a science. Normally, there are discrepancies between conceptual cost estimates and project schedules which are planned later. The differences between these two different cost figures can have serious consequences:

- Estimate too high:

- you could lose the bid (or budget approval)

- you could waste money (Parkinson's Law - "Work expands to fill the time allowed.")

- Estimate too low:

- you could lose money on a hard dollar contract

- you risk overrunning the budget

In an ideal situation, cost estimating and project planning will match up in a one to one relationship. The only way to achieve this consistently is to actually base cost estimates upon detailed plans/schedules.

Accurately forecasting the cost of future projects is vital to the survival of any business. Cost estimators develop the cost information that business owners or managers need to make a bid for a contract or to decide whether a proposed new product will be profitable. They also determine which endeavors are making a profit.

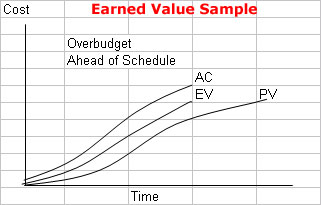

In some cases diagraming is quite helpful in understanding project costs. Below is a diagram that shows estimated cost for completion based on expenses to date:

Earned Value Reporting

As noted, the purpose of cost management is to control costs and take corrective action when necessary. A commonly used tool for measuring the budget as compared to the project schedule is called Earned Value Reporting. Earned value reporting measures the value of work performed to date and assesses if the costs are on budget and on time according to the baseline originally set. Earned value reports are cumulative, meaning current values are added to the total of all past values. Earned value reporting is based on three measurements:

- Budgeted cost of work scheduled (BCWS) also known as planned value (PV) - Planned cost of the total amount of work scheduled to be performed by the milestone date.

- Actual cost of work performed (ACWP) also known as actual cost (AC) - Cost incurred to accomplish the work that has been done to date.

- Budgeted cost of work performed (BCWP) also known as earned value (EV) - The planned (not actual) cost to complete the work that has been done.

If the budget is on track then all three of these number should be the same. When there are significant differences there is cause for concern. Here is a sample earned value chart: